*/

In Part 1 of this series, I reflected on how ‘it won’t happen to me’ is often relied upon to justify discounting financial protection. Pensions suffer a similar fate: ‘Retirement is ages away, I’ll worry about that in the future.’ The pensions landscape is continually evolving and we are becoming increasingly responsible for our retirement, which quickly comes around.

Planning a successful retirement is hard – the future is uncertain, quantifying the need isn’t an exact science and you have to balance saving with enjoying today. Do you need to change your savings plans to help you reach your goals? Here’s an example of what level of income pa is required for a single person (in today’s money), for different levels of retirement lifestyle:

State pension provision falls significantly short of what’s required. It might be available to those currently at state pension age, but there is nothing to say this will be the case in the future. You cannot rely on it to provide you with a retirement income.

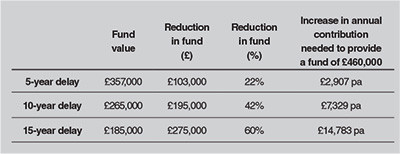

Albert Einstein observed: ‘The most powerful force in the universe is compound interest.’ Are you using it? The pension rules are clear: we have a choice of how much we can contribute and when. To put it another way: we have a choice of what we can do in retirement and when it can start. The key decision is when we start saving. The earlier you start, the easier it is to create the retirement lifestyle you want. If you were to invest £10,000 pa to a Registered Pension Scheme from age 30, subject to assumptions below, a projected fund of £460,000 would be available at age 60. A delay in your savings plan can have significant impact on this (see table).(2)

As self-employed sole traders, barristers can establish personal defined contribution pensions. These are different to other investment plans – contributions are boosted by tax relief. When you pay eligible contributions into a pension, the government tops it up – tax relief at basic rate is applied automatically and tax relief above this is claimable via your self-assessment. It is not often a policy favours higher earners. So, where affordable, it would be foolish not to benefit from it, while simultaneously planning for your future.

With frequent changes in legislation around pensions, comes complexity. There is an ‘annual allowance’ on the amount of contributions on which you can benefit from tax-relief now as much as £60,000 per annum, but… this is subject to your annual taxable income, the tapering rules applying.

Following the 2015 Pension Freedoms, you now have greater choice as to how to access your pension once you reach 55 (rising to 57 in 2028). Gone are the days when you had to purchase an annuity. While it might still be the right solution, all options should be considered to determine the one best suited. However, with this new-found freedom and control comes additional risks – most significantly, how you manage your retirement income so that it doesn’t run out. Working with an adviser and engaging with your retirement plans right from the start, provides you with peace of mind you’re protecting your future in your youth and enjoyment from a comfortable retirement lifestyle when you get there.

Book your no-obligation financial protection health check with Westgate today:

References: (1) The Pensions and Lifetime Savings Association/Loughborough University, Retirement Living Standards. (2) This example makes a number of assumptions: The average annual investment growth before charges is 4.61% each year. Investment charges of 1.96% each year. Contributions are invested on the same day in each year in a pension and are shown before charges are taken into account. The example is only an illustration and actual investment returns make be more or less than those assumed in the illustration. Please note that these benefits are not guaranteed. Benefits depend on how the investment grows and its tax treatment. Contributions are not limited by the Annual Allowance or by earnings.

SJP Approved 20/06/2024

Westgate Wealth Management Ltd is an Appointed Representative of and represents only St. James’s Place Wealth Management plc (which is authorised and regulated by the Financial Conduct Authority) for the purpose of advising solely on the group’s wealth management products and services, more details of which are set out on the group’s website www.sjp.co.uk/products. The St. James’s Place Partnership and the titles ‘Partner’ and ‘Partner Practice’ are marketing terms used to describe St. James’s Place representatives.

Louise Crush is a Chartered Financial Adviser at Westgate Wealth Management, Senior Partner Practice of St. James’s Place. Called to the Bar in 2015, Louise has built a specialist practice advising members of the Bar nationally and provides financial education services for chambers.

Westgate Wealth Management Limited is an Appointed Representative of and represents only St. James’s Place Wealth Management plc (which is authorised and regulated by the Financial Conduct Authority) for the purpose of advising solely on the group’s wealth management products and services, more details of which are set out on the group’s website www.sjp.co.uk/products. The St. James’s Place Partnership and the titles ‘Partner’ and ‘Partner Practice’ are marketing terms used to describe St. James’s Place representatives.

In Part 1 of this series, I reflected on how ‘it won’t happen to me’ is often relied upon to justify discounting financial protection. Pensions suffer a similar fate: ‘Retirement is ages away, I’ll worry about that in the future.’ The pensions landscape is continually evolving and we are becoming increasingly responsible for our retirement, which quickly comes around.

Planning a successful retirement is hard – the future is uncertain, quantifying the need isn’t an exact science and you have to balance saving with enjoying today. Do you need to change your savings plans to help you reach your goals? Here’s an example of what level of income pa is required for a single person (in today’s money), for different levels of retirement lifestyle:

State pension provision falls significantly short of what’s required. It might be available to those currently at state pension age, but there is nothing to say this will be the case in the future. You cannot rely on it to provide you with a retirement income.

Albert Einstein observed: ‘The most powerful force in the universe is compound interest.’ Are you using it? The pension rules are clear: we have a choice of how much we can contribute and when. To put it another way: we have a choice of what we can do in retirement and when it can start. The key decision is when we start saving. The earlier you start, the easier it is to create the retirement lifestyle you want. If you were to invest £10,000 pa to a Registered Pension Scheme from age 30, subject to assumptions below, a projected fund of £460,000 would be available at age 60. A delay in your savings plan can have significant impact on this (see table).(2)

As self-employed sole traders, barristers can establish personal defined contribution pensions. These are different to other investment plans – contributions are boosted by tax relief. When you pay eligible contributions into a pension, the government tops it up – tax relief at basic rate is applied automatically and tax relief above this is claimable via your self-assessment. It is not often a policy favours higher earners. So, where affordable, it would be foolish not to benefit from it, while simultaneously planning for your future.

With frequent changes in legislation around pensions, comes complexity. There is an ‘annual allowance’ on the amount of contributions on which you can benefit from tax-relief now as much as £60,000 per annum, but… this is subject to your annual taxable income, the tapering rules applying.

Following the 2015 Pension Freedoms, you now have greater choice as to how to access your pension once you reach 55 (rising to 57 in 2028). Gone are the days when you had to purchase an annuity. While it might still be the right solution, all options should be considered to determine the one best suited. However, with this new-found freedom and control comes additional risks – most significantly, how you manage your retirement income so that it doesn’t run out. Working with an adviser and engaging with your retirement plans right from the start, provides you with peace of mind you’re protecting your future in your youth and enjoyment from a comfortable retirement lifestyle when you get there.

Book your no-obligation financial protection health check with Westgate today:

References: (1) The Pensions and Lifetime Savings Association/Loughborough University, Retirement Living Standards. (2) This example makes a number of assumptions: The average annual investment growth before charges is 4.61% each year. Investment charges of 1.96% each year. Contributions are invested on the same day in each year in a pension and are shown before charges are taken into account. The example is only an illustration and actual investment returns make be more or less than those assumed in the illustration. Please note that these benefits are not guaranteed. Benefits depend on how the investment grows and its tax treatment. Contributions are not limited by the Annual Allowance or by earnings.

SJP Approved 20/06/2024

Westgate Wealth Management Ltd is an Appointed Representative of and represents only St. James’s Place Wealth Management plc (which is authorised and regulated by the Financial Conduct Authority) for the purpose of advising solely on the group’s wealth management products and services, more details of which are set out on the group’s website www.sjp.co.uk/products. The St. James’s Place Partnership and the titles ‘Partner’ and ‘Partner Practice’ are marketing terms used to describe St. James’s Place representatives.

The age of criminal responsibility, extreme weather and conflict resolution – plus, new protocol for reporting bullying at the Bar

By David Green

Mário Barroso, Head of R&D and Method Development at AlphaBiolabs, examines the forensic science underpinning hair drug testing, its evidential scope and limitations, and why it remains the gold standard for evidencing patterns of drug use in family proceedings

Unlocking your aged debt to fund your tax in one easy step. By Philip N Bristow

Clement Cowley, Partner at The Penny Group, discusses the upcoming changes to pensions and Inheritance Tax and the potential impact on your financial future

Save the Children UK is the latest charity to benefit from a £500 donation from AlphaBiolabs via the company’s Giving Back initiative

Barrister apprenticeships – shortly to provide the fourth pathway to the Bar – are an ideal opportunity to support local talent and ‘grow your own’, say Tim Coulson and Dr Jane Dennehy

Solicitor General Ellie Reeves KC MP discusses her decade as a trade union and employment law barrister, the demands of life as a Law Officer and the number one priority shaping her work. Interview by Anthony Inglese CB

A decade of reviews and research has disrupted accepted thinking in the search for causality. Suicides following abuse have overtaken domestic homicides. Is the law keeping up? Professor Susan Edwards KC (Hon) examines recent cases and the obstacles to successful prosecution

Why every major sporting event needs an anti-corruption policy. By Louis Weston

At least not that way, says Richard Paige